Let me paint a picture. You're a Micron employee. You've been gradually collecting RSUs, reinvesting in your company, and watching the stock do... fine. Decent. Nothing to write home about. Then, seemingly overnight, everything changes. Your net worth jumped in a way that feels almost unreal, and now you're staring at a brokerage account wondering what on earth to do next.

If that's you, this one's for you.

And if you work for a different company with a similar stock run-up, or you've been half-paying attention while your colleagues quietly panic about taxes, stick around. The concepts here apply broadly.

Jump to what you're looking for:

You probably don't need us to explain why Micron stock has been on a historic run. You've been watching it happen from the inside. The short version for anyone catching up: AI created an insatiable demand for High Bandwidth Memory (HBM), Micron became a premier supplier, and MU went from roughly $85 in early 2024 to new all-time highs.

No one knows where MU goes from here. Anyone who tells you otherwise is probably selling something. What we can control is how you respond to where you are today.

Most Micron employees with stock compensation fall into one of two camps:

This article focuses on how to manage the tax impact, because that's where we can make a real difference.

This is one of the most common questions we hear, so let's answer it clearly.

At vesting: When your RSUs vest (become yours), the fair market value of those shares is reported as ordinary income on your W-2, taxed just like your salary. You've likely already paid taxes on that piece through payroll withholding.

Important caveat: Most employers only withhold at the standard 22% supplemental wage rate, which is often lower than your actual tax bracket as a high earner. That gap can create a surprise tax bill in April if you're not proactive about it.

After vesting, when you sell: Any increase in value above the price on your vest date is a capital gain.

For many dual-income couples in Boise with combined incomes over $500K, the long-term rate works out to 18.8% - 23.8% federal. Still far better than ordinary income rates, but it adds up fast on a large position.

This is the question everyone's sitting with. And although now would be a really good time for a crystal ball, the next best thing is an honest, data-driven answer.

If you're holding a concentrated position in any single stock, including one you love and work for, you're accepting a level of risk the data says most investors shouldn't. Historically, only about one in five stocks survives and outperforms the market over 20-year periods.¹ Roughly 4% of stocks have generated essentially all of the net wealth created by the U.S. stock market. The other 96% either barely kept pace or destroyed value.²

We often compare holding a single stock to gambling, because in a sense that's what you're doing. You're making a bet that yours will be one of the lucky few. Our job is to take the emotion out of it and put the odds in your favor.

So the question we should really be asking isn't "will MU keep going up?" It's: "What are the realistic odds that Micron continues to outperform a diversified portfolio over the next 10, 20, 30 years?" Honestly? Low. Not impossible, but unlikely, and the longer your time horizon, the less likely it gets.

One exercise we do with clients is a simple comparison: how much does Micron's stock price have to drop before your paper loss exceeds the taxes you'd owe by selling today?

The answer almost always surprises people, because the break-even decline is much smaller than they expect.

Single stocks are significantly more volatile than a broadly diversified portfolio. Historically, the 20th percentile return for an individual U.S. stock in a given year has been around -29.4%.³ Even in normal years, a meaningful chunk of stocks drop 20 to 30% or more. That's just part of the ride when you're concentrated in one name.

Here's a concrete example. Let's say you own $400,000 of Micron stock, of which $300,000 is long-term capital gain. Assuming a combined federal and Idaho marginal rate, you'd owe approximately $87,300 in tax if you sold everything today, leaving you with roughly $312,700 after tax, now fully diversified.

Alternatively, if you hold and the stock drops just 20%, a completely normal single-stock outcome, your position is worth $320,000. On the surface that looks better. But you still have an embedded tax liability on that $320,000, and you're still fully concentrated in one company. You're not really better off, and you've taken on all the downside risk to get there.

Now zoom in: if MU drops just 5%, your position loses $20,000 in value. But you would've paid only about $6,000 in taxes to sell that piece and diversify. You gave up $20,000 in value to avoid a $6,000 tax bill. That math rarely makes sense, and it's the kind of thing that's easy to miss when you're focused on the tax number in isolation.

We're happy to run this with your actual numbers. It's one of the most clarifying conversations we have, and it takes about 15 minutes. Book a free call with us.

Here's where it gets genuinely fun, and where working with a CFP® professional who's also a CPA really pays off. These strategies can be layered to dramatically reduce your tax bill in the year you sell.

Every dollar you defer into a pre-tax retirement account reduces your taxable income, which lowers the effective rate at which your stock gains are taxed. For a dual-income household, this can add up quickly if you are both taking full advantage of what is available to you.

2026 contribution limits:

*Important caveat: The $24,500 employee contribution limit is per person across all 401(k) plans, not per plan. But Solo 401(k)s also allow employer contributions of up to 25% of net self-employment income, which is separate from that limit. So, someone with both a W-2 job and self-employment income can max the employee contribution at work, capture the full employer match, and still stack Solo 401(k) employer contributions on top, up to a $72,000 combined total across all 401(k)s in 2026.

Thanks to the One Big Beautiful Bill Act of 2025, high earners can now deduct up to $40,000 in state and local income and property taxes, up from the old $10,000 cap.⁴ This phases out between $500K and $600K of income.

Why this matters specifically for Micron employees: Many couples in Boise are approaching or near that $500K threshold after factoring in RSU vests and a spouse's income. Strategic timing of when you sell stock, or how you structure other deductions, can keep you in the range where you capture the full $40K SALT benefit. That's a $30,000 swing in deductions compared to the old law. Huge benefit when properly planned for.

If you have a taxable brokerage account, two moves can reduce your ongoing tax drag without changing your overall investment strategy.

Asset location. Think of this as putting the right investments in the right accounts:

Tax-loss harvesting. When other positions in your brokerage account are at a loss, selling them locks in a tax loss you can use to offset your Micron gains. You immediately reinvest in a similar (but not identical) fund so you stay invested. The IRS wash-sale rules require careful execution here, and it's one of the areas where having an experienced advisor managing your portfolio can be quite valuable.

If charitable giving is already part of your life, whether that's tithing, your local church, or community causes, this is the year to be strategic about how you give. You can accomplish exactly what you'd planned to give anyway, while making the tax bill dramatically lower.

Option A: Donate appreciated MU shares directly to a charity. Instead of writing a check or giving cash, donate the actual shares. The charity receives the full value, you avoid all capital gains tax on the donated portion, and you get a charitable deduction for the full fair market value (subject to 30% of AGI, with a 5-year carryforward). Both you and the charity come out ahead compared to a cash donation.

Option B: Contribute appreciated MU stock to a Donor-Advised Fund (DAF). This is one of our favorite tools for high-income years. Here's how it works:

The DAF perfectly matches the timing of your big tax event with a large deduction. In the illustrative example below, this single move generates over $97,000 in additional deductions.

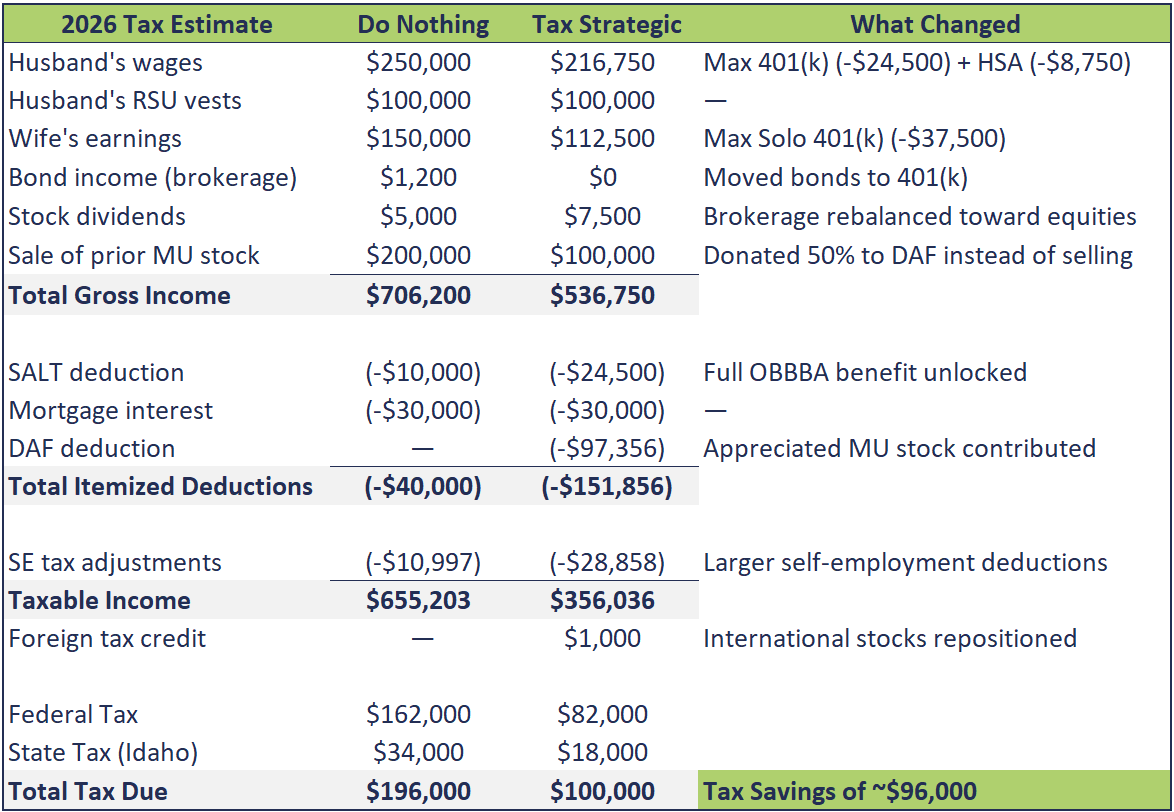

Here's an example of a client profile we often see.

Purely hypothetical for illustrative purposes.

Meet the Millers, late 30s, Boise, Idaho:

Do Nothing vs. Get Strategic

Total Tax Savings: ~$96,000 in a Single Year

That's not a typo. And the Millers aren't doing anything exotic. They're maxing their retirement accounts, moving bonds to the right accounts, giving to charity using appreciated stock instead of cash (something they were going to do anyway), and timing their stock sale with a DAF contribution.

Every single one of these moves is available to you.

And $96,000 isn't just a number on a spreadsheet. It's adown payment on a rental property. It's a fully-funded college account. It's years of compounding growth that otherwise goes to the government. These strategies paid for a financial advisor many times over, with a single year's planning.

Taxes are just the beginning of the conversation.

If you have Micron stock compensation, you may be sitting on a once-in-a-career opportunity to dramatically accelerate your financial trajectory. To reach financial independence sooner than you ever thought possible, pay off debt, fund your kids' educations, or simply get to the point where work is a choice rather than a necessity.

That doesn't happen by accident. It happens with a plan.

A thoughtful financial plan built around your specific Micron compensation, your family's goals, and Idaho's tax environment doesn't just save you money this year. It gives you clarity, confidence, and a whole lot less Sunday-night anxiety about whether you're making the right calls with what you've earned.

→ Schedule a free conversation with Vitality Wealth

Q: How much tax will I owe when my Micron RSUs vest? At vesting, you'll owe ordinary income tax on the fair market value of the shares received. For many high-earning Micron employees in Idaho, that can be up to 37% federal + 5.3% Idaho state = roughly 42 to 43% combined marginal rate. Your employer withholds taxes at vesting, but typically only at the 22% federal supplemental rate, meaning you'll likely owe more at tax time than what was withheld. Plan for this with quarterly estimated payments or increased withholding on regular wages if needed.

Q: Should I sell my Micron RSUs immediately when they vest? In most cases, yes, and here's our honest reasoning. Holding concentrated employer stock is a risk most financial planners would advise against, especially when the position is already large. Selling at vest and diversifying eliminates future capital gains exposure and puts the investment odds in your favor. If you feel strongly about maintaining some Micron exposure, a reasonable rule of thumb is keeping single-stock positions to around 5% of your overall portfolio.

Q: What is the capital gains tax rate on Micron stock in Idaho? For long-term capital gains (held more than one year after vesting), the federal rate is 15 to 20% depending on income, plus 3.8% NIIT if your combined income exceeds $250K (married filing jointly). Idaho taxes capital gains at the same flat rate as ordinary income, currently 5.3%, with no preferential state rate for long-term gains. Combined, high-earning Idaho residents typically pay 24 to 29%+ on long-term MU stock gains.

Q: Can I avoid capital gains tax on Micron stock by donating it? Yes. Donating appreciated Micron shares directly to a qualified charity or Donor-Advised Fund lets you avoid capital gains tax entirely on the donated portion, while still receiving a charitable deduction for the full fair market value. If you're already planning to give, this is one of the most impactful tax moves available to you.

Q: What is a Donor-Advised Fund and how does it work for Micron employees? A Donor-Advised Fund is a charitable giving account where you contribute appreciated assets like Micron stock, receive an immediate tax deduction, and then recommend grants to charities over time at your own pace. The assets are sold inside the DAF tax-free and invested while you decide where they go. It's especially powerful in a high-income year when you want a large deduction now but flexibility in your giving later.

Q: Is there a financial advisor in Boise that specializes in Micron stock compensation? Yes — that's us. Vitality Wealth is a fiduciary, fee-only financial planning firm in Idaho working specifically with high-earning professionals navigating complex compensation, including Micron RSUs, equity tax planning, and building a clear path to financial independence. We'd love to connect.

¹ Dimensional Fund Advisors, "Singled Out: Historical Performance of Individual Stocks," Wes Crill, PhD

² Bessembinder, "Do Stocks Outperform Treasury Bills?" Journal of Financial Economics, 2018

³ Dimensional Fund Advisors, "Magnifying Single-Stock Volatility," Wes Crill, PhD

⁴ One Big Beautiful Bill Act, Pub. L. No. 119-21, signed into law July 4, 2025.