The One Big Beautiful Bill Act (OBBBA), signed into law on July 4, 2025, brings the most significant tax law update since the 2017 Tax Cuts and Jobs Act. Some parts extend previous tax cuts, while others bring new rules that could impact your deductions, your business income, and even your charitable giving strategy.

If you’re a business owner, medical professional, or high-income household, many of these changes could directly impact your tax situation.

Below, we walk through the major changes from OBBBA—what changed, who it affects, and why it matters. And, since reading tax law isn’t everyone’s cup of tea (😊), we’ve separated this into two sections: for the light readers and for the deep divers.

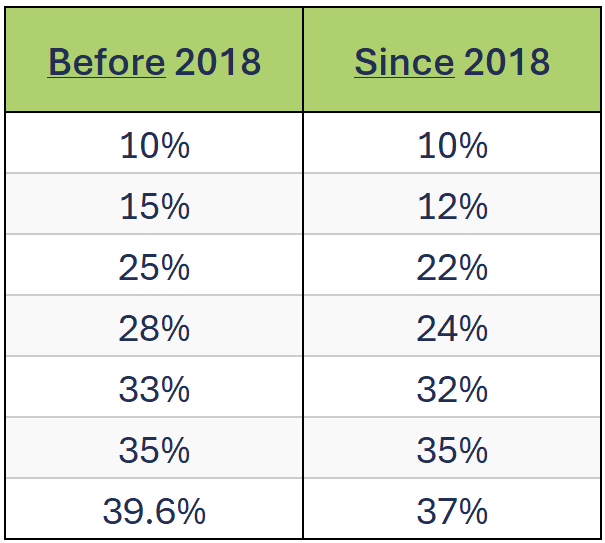

What: This is the biggest change that will affect the most people, but it’s easy to overlook because it won’t feel like a change. Back in 2018, tax brackets were lowered across the board. Before this new tax bill, those lower tax rates were scheduled to “expire” at the end of 2025 and revert to the higher pre-2018 rates. OBBBA makes the lower rates we’ve had for the past several years permanent (until Congress passes a new law to change them again).

Who: Everyone!

Why it matters: Your tax rates are no longer scheduled to go up in January 2026, which means lower taxes for essentially everyone. If you’re doing long-term planning (like Roth conversions, charitable giving, retirement income projections), this change provides more clarity for the next few years.

_________________________________

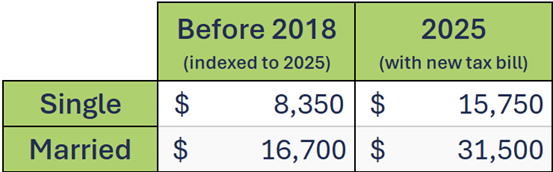

What: In 2018, the standard deduction was significantly increased. Like many changes from that year, it was set to expire in 2026 and revert to about half the current amount. The good news: that higher deduction has now been made permanent.

Who: Everyone, but especially those over age 65 (now and in the next 4 years).

Why it matters: Less income is taxed, and fewer people need to itemize.

🔷 Think about: Whether itemizing still makes sense for your situation, or if you should “lump” deductible expenses into every other year to exceed the standard deduction.

________________________________________

What: If you itemize deductions, the amount you can deduct for state, local, and property taxes (SALT) has increased dramatically, from $10k to $40k. If your income (MAGI) is over $600k (single or married), then you are stuck with the $10k cap. If your income (MAGI) is between $500k-$600k then you will get a prorated amount between $10k-$40k, depending on your income.

Who: Households who make over $300k, own a home, and itemize deductions. This is especially impactful for those in high-tax states (e.g., CA, NY, NJ).

Why it matters: If you pay significant property taxes or state income taxes, this could save you several thousand dollars each year.

🔷 Think about: If your income is between $500k–$600k, it may be worth exploring tax planning strategies to reduce your MAGI below $500k to qualify for the full deduction.

________________________________________

What: Since 2018 many business owners and independent contractors have benefited from a 20% deduction on qualified business income (QBI). This deduction was set to “expire” and be eliminated, but is now “permanent”. They also expanded the eligibility to include those with taxable income up to $275k (single) and $550k (married).

Additionally, there were no changes or restrictions on pass-through entities (PTEs) like LLCs and S-Corps. Many business owners benefit by running personal income through their business entity, which in some states allows them to avoid the SALT cap described above. While lawmakers considered limiting this benefit, OBBBA left it fully intact.

Who: Business owners and self-employed professionals—including physicians, dentists, consultants, and independent contractors.

Why it matters: A major tax benefit remains available for small business owners. With the expansion, it’s possible you will qualify now, even if you didn’t before.

🔷 Think about: Rechecking your eligibility if your business income was previously too high. Also worth reviewing your entity structure to optimize for both QBI and SALT planning.

________________________________________

What: Good news first! If you don’t itemize on your tax return (meaning you take the standard deduction), you can now deduct up to $2,000 in gifts to charities each year. Previously, only those who itemized could benefit from charitable donations.

Now for the less good news. If you already itemize and make charitable donations, you won’t be able to count the entire amount of your charitable donations. Beginning in 2026 there will be a “hurdle” of 0.5% of your income (AGI). For example, if your AGI is $300k and you donate $30k/yr to your church, you won’t be able to count the first $1.5k (0.5% of AGI) towards your itemized deductions. You would only be able to count $28.5k of your $30k donation.

Who: Anyone who gives to charity

Why it matters: Standard deduction filers now get a small charitable deduction, but those who donate large amounts may lose a small amount of the tax benefit they receive from itemizing.

🔷 Think about: Making a large charitable contribution to a Donor-Advised Fund (DAF) in 2025 before the new rule takes effect in 2026.

________________________________________

What: Credits for solar panels, energy efficiency home improvements (insulation, HVAC, doors, windows, etc.), electric cars, and chargers are going away. Some credits go away as soon as the end of September 2025, while others aren’t eliminated until July 2026.

Who: Homeowners, buyers, installers, and sales professionals of clean energy tech

Why it matters: You will miss out on these savings if you wait.

🔷 Think about: Acting now if you were already planning a solar or EV purchase. Same goes for energy efficient home improvements.

________________________________________

Whether you’re a practice owner, retiree, or busy professional, these tax law changes could have a meaningful effect on your bottom line. The good news is that many key deductions and tax rates have been made permanent, but there are also new limitations that may require a proactive approach, especially when it comes to charitable giving and SALT planning.

At Vitality Wealth, we help clients navigate these changes and translate tax law into practical decisions for their long-term tax strategy.

What: The credit goes from $2,000 to $2,200+ per child, with annual increases. Again, this seems super minor, but without the new legislation, the credit would have dropped back to $1,000 per child.

Who: Parents with children under age 17.

Why it matters: You’ll owe less tax each year for each child.

🔷 Think about: Having more children to get more tax credits… kidding! There are many great reasons to have kids, but getting a larger tax credit doesn’t exactly offset the other costs. 😊

________________________________________

What: Under the 2017 Tax Cuts and Jobs Act, business owners could immediately deduct (instead of depreciating over many years) the full cost of qualifying assets like equipment, computers, and certain improvements. This is called 100% bonus depreciation. Before OBBBA, this was set to phase down starting in 2023 and drop to 0% by 2027. The new law keeps 100% bonus depreciation in place through 2028.

Who: Business owners, real estate investors making qualified improvements, and anyone buying significant business assets.

Why it matters: Instead of spreading deductions over several years, you can deduct the full cost up front. This lowers taxable income today and frees up cash flow.

🔷 Think about: Timing large purchases (like equipment or renovations) while this deduction is still at 100%, especially if your business had higher profits this year.

________________________________________

What: Overtime and tip income can now be deducted from your taxes from 2025-2028. To qualify, you must work in an occupation that has traditionally received tips and the tips must not be mandatory (that’s not a tip). They specifically excluded many service professionals from lawyers, accountants, and financial advisors to artists and entertainers. Lastly, if your income (MAGI) is greater than $150k/yr (single) or $300k/yr (married), your tip deduction will start to be reduced and eventually eliminated, depending on your income.

Who: Hourly workers, restaurant employees, or anyone earning qualified tips.

Why it matters: If you receive gratuities, you might owe less tax.

🔷 Think about: Tracking this income clearly so you can take the deduction.

________________________________________

What: Similar to the tip deduction, overtime income can now be deducted from your taxes from 2025-2028. If you work overtime in your job, you can deduct up to $25k (married) or 12.5k (single) of overtime income. If your income (MAGI) is greater than $150k/yr (single) or $300k/yr (married), then your overtime deduction will start to be reduced and eventually eliminated, depending on your total income.

One nuance is that you don’t get to deduct the full amount you earned in overtime, but just the difference in your overtime rate and your regular rate. For example, if you normally earn $30/hr but get paid $40/hr for overtime, then for every hour of overtime you work you can deduct $10/hr (40/hr-30/hr).

Who: Hourly workers, service employees, or anyone earning overtime wages.

Why it matters: If you worked extra, you might owe less tax.

🔷 Think about: Tracking this income clearly so you can take the deduction.

________________________________________

What: A new type of account designed to help save for children’s future retirement. There are many specific rules—we’ll only cover the major details. Beginning in July 2026 you can contribute up to $5k/yr to the account until the child is 18 years old. The nice thing is that you can make contributions to the child’s account, even if they don’t have “earned income” from a job (which would be required for a minor Roth IRA). Unfortunately, there isn’t a tax deduction for contributing like there is for an IRA.

The Trump account can essentially only be invested in low-cost index funds that are primarily invested in US stocks (such as S&P 500). No withdrawals can be taken from a Trump account until after age 18. Once the child is 18, the account will function much like an IRA where you would be subject to early withdrawal penalties if you withdraw money before age 59 ½.

One other notable detail is that children born between 2025–2027 will receive $1k tax credit to be paid directly into Trump account. No details on how that will work or the mechanics of how it gets into the account, but it’s free money! Any contributions from government organizations and charities don’t count towards the $5k/yr contribution limit.

Who: Families with minor children, especially those with a newborn in 2025 or who plan to have children in the next couple of years.

Why it matters: Can be a way to jumpstart savings for a child’s future, plus you might be eligible for a free $1k from the US government.

🔷 Think about: Opening and contributing to one if your child is eligible — especially if they were born in 2025.

________________________________________

What: 529 plan money can now be used tax-free for certain K–12 expenses (not just tuition), professional credentials, and career training. Not all expenses are eligible, but many new costs are eligible: including AP exams, textbooks, tutoring, ACT/SAT exams, dual enrollment classes, and therapy for disabilities. They are also increasing the limit from $10k/yr for K-12 expenses to $20k/yr.

Who: Parents, grandparents, or anyone with a 529 education account.

Why it matters: More flexibility in how you use your 529 plan and get tax-free withdrawals

🔷 Think about: Adjusting 529 contributions if you want to cover private school or professional certifications.

________________________________________

What: The alternative minimum tax (AMT) is very complicated. At a high level, it’s a completely separate tax system that is meant to make sure that wealthier taxpayers at least pay a minimum amount of tax and don’t benefit too much from a bunch of tax deductions. AMT has existed for decades, but over the past few years it was changed so that it only affected a small percent of taxpayers.

This new bill lowers the dollar amount that is exempted from AMT, meaning more people may be subject to it.

Who: Big for individuals who receive equity compensation and incentive stock options (ISOs). Also may affect higher-income households ($500k-1M+) with lots of deductions.

Why it matters: Your tax calculation may need to be run two ways — and the AMT could apply.

🔷 Think about: Talking with your CPA if your income is high and you rely on big deductions.

________________________________________

What: Private mortgage insurance (PMI) counts as mortgage interest and can be deducted. This hasn’t been the case for the past couple of years and is a nice break for those who pay PMI.

Who: Homeowners who didn’t put 20% down and are paying PMI.

Why it matters: You can now write this off if you itemize your deductions, lowering your taxes.

🔷 Think about: Reviewing your mortgage documents to see if you qualify for this deduction.

________________________________________

What: You can deduct up to $10,000 in interest on a “qualifying” U.S. car loan. You must meet several criteria to qualify—the big ones being that the vehicle must be for personal use (not business), weigh less than 14,000 lbs, and be assembled in the United States. This is only in effect from 2025-2028 and only counts for cars purchased after 12/31/2024.

Who: Car buyers who financed a vehicle with a qualifying loan.

Why it matters: Buying a car with a loan may now come with a tax break.

🔷 Think about: Keeping records of your loan interest and including it in your tax prep.

________________________________________

What: Estate and gift tax will continue to apply to a small fraction of Americans. You can now transfer (through gift or inheritance) $15M (single) or $30M (married) without tax.

Who: High-net-worth individuals and families, especially business owners.

Why it matters: More wealth can be passed down tax-free.

🔷 Think about: Updating your estate plan or making large gifts now that the exemption is higher.

________________________________________

What: If you’re in the 37% bracket, meaning your taxable income is above $626k (single) or $751k (joint), then your itemized deductions will be worth a little less. In the past if you were in the 37% tax bracket, then every $1 of additional income resulted in an additional $0.37 of tax. Likewise, every $1 of itemized deductions (like charitable donations or state/local taxes) was worth $0.37 in tax savings (by showing less income).

The government decided to add an extra layer of complexity to slightly increase taxes. Now if you are in the 37% tax bracket then $1 of income still results in $0.37 in tax paid, BUT $1 of itemized deduction only results in $0.35 tax savings. Said differently, when you are in the 37% tax bracket then your itemized deductions are only worth 35% (not 37%).

Who: Very high-income earners.

Why it matters: Slightly reduces your benefit from deductions and increases your total taxes paid.

🔷 Think about: Whether your strategy for giving or state tax timing should be adjusted.

________________________________________

What: Originally available in 2018, these real estate opportunity zones will continue to be available. These are low-income areas that the local governments designate as opportunity zones. If you invest in real estate in these areas, then you can defer or reduce capital gains that you have from your other investments. We won’t go into all the specifics here, but the key is that these qualified opportunity zones will continue to exist and can offer tax benefits to investors for investing in low-income areas.

Last important note is that this extension does NOT extend the 2026 timeline for those who already own qualified opportunity zone investments. Those original investors still will see their tax deferral end in 2026, at which point they will need to pay taxes on their capital gains.

Who: Real estate investors who are looking to defer or reduce capital gains. Also important for investors who already own qualified opportunity zone property.

Why it matters: Can be a good way to reduce taxes on appreciated investments, but requires a concentrated investment into directly held real estate.

🔷 Think about: If you already own opportunity zone property then you should consider other ways to defer or offset your impending 2026 tax bill.

________________________________________

These sweeping changes from the OBBBA present both opportunities and complexities, especially for business owners, medical professionals, and high-income families. With many key provisions now made permanent, and others set to expire in just a few years, proactive planning is more important than ever. Whether it’s reevaluating your charitable giving strategy, optimizing your business deductions, or navigating new deduction limits, these updates can significantly affect your long-term tax picture. If you’re unsure how these changes apply to you, we’re here to help translate the law into clear, personalized guidance. Reach out to schedule a conversation and explore how we can align your tax strategy with your broader financial goals.